The Paycheck Protection Program of the CARES Act goes live today (though lenders are expressing concern about preparedness). This post is intended for religious nonprofits that have questions about the strings attached to governmental aid. What rights will they relinquish as a condition of accepting a government-guaranteed, forgivable loan?

These concerns are rooted in the language of the loan application itself as well as certain federal regulations that may be triggered by acceptance of federal financial assistance.

The Paycheck Protection loan application, SBA Form 2483, includes the following language:

There was hope that the SBA regulations would address religious liberty concerns, but in its interim final rule released on April 2, the SBA punted:

While we wait for additional guidance from the SBA, here is some preliminary analysis regarding religious preferences and regulatory burdens.

RELIGIOUS PREFERENCES IN EMPLOYMENT

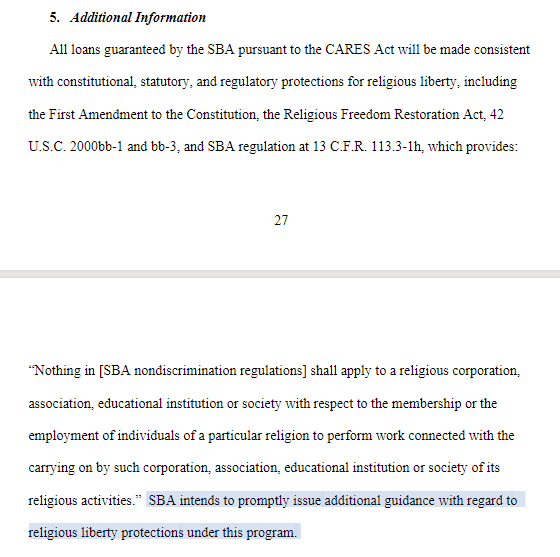

Existing SBA regulations are no more restrictive than current federal and state fair employment laws regarding preferring employees on the basis of religious belief and conduct. The SBA regulations at 13 CFR 113.3-1(h) provides that: “Nothing in this part [regarding SBA loans and nondiscrimination] shall apply to a religious corporation, association, educational institution or society with respect to the membership or the employment of individuals of a particular religion to perform work connected with the carrying on by such corporation, association, educational institution or society of its religious activities.” The SBA regulations define “religion” as “all aspects of religious observance and practice, as well as belief.”

These regulations are modeled on Title VII of the Civil Rights Act, meaning that any religious nonprofit with 15 or more employees is already subject to similar laws regarding employment preferences. And though the text of the Washington Law Against Discrimination has a broader religious exemption, it has been interpreted more narrowly and is the subject of a current appeal pending before the Washington Supreme Court. Bottom line: as a practical matter, SBA regulations are no more restrictive than existing law on employment discrimination.

PUBLIC ACCOMMODATION

The public accommodation issue is a little harder. The SBA regulations at 13 CFR 113.3(a) prohibit discrimination in places of public accommodation, and there is no religious exemption. If acceptance of a PPP loan established a nonprofit organization as a place of public accommodation, this could potentially be an issue in primary and secondary schools, for example, that require students to agree with the school’s statement of faith. In contrast, religious schools are not considered places of public accommodation under existing state or federal law.

Receipt of federal financial assistance can also trigger Section 504 of the Rehabilitation Act, which prohibits discrimination on the basis of disability in programs receiving federal financial assistance. Private religious schools are again the most likely to be impacted by this requirement, as they often lack the resources to accommodate students with significant disabilities and are otherwise exempt from the ADA and state law regarding public accommodation. Still, the regulations under 504 only require the recipient of federal financial assistance to make “minor adjustments” to accommodate a disabled student.

HOW LONG DO FEDERAL REGULATIONS APPLY?

The duration of “federal financial assistance” depends upon the statute at issue, but it is reasonable to conclude that an organization would be deemed a recipient during the time the loan is pending because it remains guaranteed by the federal government. If the loan is forgiven after eight weeks, this is a short duration. If the loan is not forgiven, the interim final rule released by the SBA provides for a two-year repayment term.

BOTTOM LINE

Given that the program is first-come, first-served, and lenders will be overwhelmed, organizations that would otherwise be interested in a paycheck protection loan should not wait to apply. Get the application in, consider the organization’s programming in light of the above potential restrictions, and stay tuned for the promised additional guidance from the SBA.